![]()

502 Bank Street Decatur, AL 35601 T/F (256) 850-4161

A Little Distress Selling

By Paul Lamont

August 23, 2007

It looks as if the Summer of 1929, has finally past. We are now experiencing "forced selling and unwinding of leverage on assets" that we stated would follow. Thus begins the bull market in cash.

“There are three faithful friends: an old wife, an old dog, and ready money.” - Benjamin Franklin

Forced Selling Due To Margin Calls

As The Telegraph reports:

“‘Everyone has hiked margin calls and anyone who says they haven't is lying,’ said one banker...‘This is a one-in-a-100-year event in which there are extremely unusual correlations that no one prepared for,’ warned one banker. ‘We are in a situation where everyone is very scared.’”

Actually, it's more like every 60 years. The Panic of 1837, 1875, 1929 and now

2007 are all ‘End of the Credit Boom’ events. The final result is the wipeout

of leverage/debt in the economy.

Market Breakdown

From our April 19th report: “Astute chart watchers have recognized that markets follow elliptical curves. Currently, we are finishing up an ellipse that started in October of 2005…When price snaps out of this ellipse, the DJIA will be pursuing a new direction: down or sideways. Of course, readers know our bias is down. We believe the decline will be swifter than February’s sell off.” The chart below shows the recent plunge:

One historical characteristic of a bear market is its amazing volatility, especially the dramatic rallies. For instance in John Kenneth Galbraith’s The Great Crash: 1929, he reflects: “Still, in its own way, the recovery on Black Thursday was as remarkable as the selling that made it so black. The Times industrials were only off 12 points, or a little more than a third of the loss of the previous day.” On Black Thursday, “Montgomery Ward, which had opened at 83 and gone to 50, came back to 74.” End-of-the-day recoveries that occur after huge intraday drops (August 16th) are merely marking short-term lows and should be viewed as normal as the bear market cuts lower.

Fed Injections

On Monday, it was reported that the Fed had been providing short term cash from the discount window for the balance sheet of Deutsche Bank. Two days later, Citigroup, J.P. Morgan Chase, Bank of America, and Wachovia all said they had borrowed $500 million each. According to Foundations of Financial Markets and Institutions by Fabozzi, Modigliani and Ferri; “Banks temporarily short of funds can borrow from the Fed at its discount window…Continual borrowing for long periods and in large amounts is thereby viewed as a sign of a bank’s weakness” because the Fed is “the bank of last resort.” Banks are borrowing from the Fed because they can’t get the money anywhere else, not as they claim: “it is important at this time to take a leadership role in demonstrating the potential value of the Fed's primary credit facility and to encourage its use by other financial institutions.” We would not hold accounts at these financial institutions. As we warned last November as the credit boom comes to an end: “‘severe macroeconomic repercussions’ are highly likely and that ‘banking system capital’ will be impaired.” To think the Fed will prevent the credit bust is to ignore the lessons of 1929: “the Federal Reserve can print money, but it cannot create credit or confidence. ‘Money’ is therefore hoarded, by either the public or the banks themselves (if they are concerned about an increase in redemptions).”

North of the Border

U.S. investors might not be aware that the credit bust will be affecting corporate profits. According to Bloomberg:

“Bank of Montreal, Canadian Imperial Bank of Commerce and Canada's four other biggest banks agreed to work together to ensure that the C$120 billion ($113 billion) market for asset-backed commercial paper continues to `perform satisfactorily’... ‘It may indicate the banks are facing redemptions from their commercial paper funds, and are trying to reassure investors that they'll prop up money markets,’ states Genuity Capital Markets analyst Mario Mendonca.”

The asset-backed commercial paper market is vital to the fundamental economy. Forget the homeowner/consumer; the credit crunch is now attacking companies that are dependent on short-term debt. Yes, it’s also happening in the U.S. as investors “opted for the safety of Treasuries.”

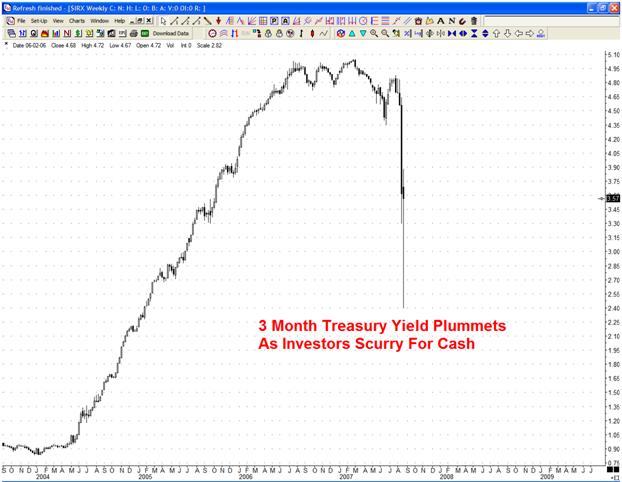

Hoarding Cash

Investors have shunned risk and rushed into U.S. Treasuries driving down the yield. The chart below shows the need to protect principal as this is the fastest move into cash since the Crash of 1987. We discussed the 20 year cycle in Seven Reasons to Sell. It also implies that investors are in denial as to the value of their leveraged assets.

The First Bank Run

Bank depositors

have also joined the rush for cash. On August 16th, the Panic of

2007 had its first bank run at Countrywide

Bank. “Anxious customers jammed the phone lines and Web

site of Countrywide Bank and crowded its branch offices to pull out their

savings because of concerns about the financial problems of the mortgage lender

that owns the bank.” According to Bill Ashmore, a depositor at

Countrywide: “‘I just don't want to deal with it. I don't care

about losing 90 days' interest, I don't care if it's FDIC-insured — I just want

it out.’” No fractional reserve bank can withstand a full redemption of their

deposits. They simply don’t have the cash on hand. At the same time, fear is

freezing up the secondary mortgage market. So if banks/funds/lenders are forced

to sell their loans for cash, they would currently find no buyers. Another interesting point is that folks are withdrawing amounts that

are over the FDIC limit and depositing them at accounts at other banks. This

creates more liabilities for the FDIC. According to their phone operators, the FDIC Deposit

Insurance Fund only has $49.5 billion. Countrywide Bank alone has

$107 Billion in assets. If there is a major bank failure the FDIC will have

to tap its credit line from the U.S. Treasury. “Printing money” will only ensure

long-term inflation and encourage riskier behavior (moral hazard).

“The Whole Town’s Gone Crazy”

To see the fearful psychology that mortgage lenders, hedge funds, and now money market funds and banks have been dealing with start at the 51 minute marker of this movie. George Bailey goes from “Float away to happy land on the bubbles” to “look we’re still in business; we still got two bucks left.” The run for cash has just started; we have a long way to go before most assets are undervalued in historical terms.

Make Sure You Have Access to Funds

As investors at Sentinel Management found out, money market funds like hedge funds can also halt redemptions. Instead, investors should be holding cash (U.S. Treasury Bills) in their own account at the most secure brokerage firms. We leave you with the words of Dr. Marc Faber on August 13th from an interview on Bloomberg:

“Basically, I think as an investor the most important (thing) is that you have patience…that you can wait for really lifetime buying opportunities and they don’t present themselves everyday. My feeling is the best, is to hold Treasury Bills and U.S. Dollars and not try to make money but try to avoid losing money.”

At Lamont Trading Advisors, we are liquidating historically overvalued assets and purchasing liquid U.S. Treasury Bills for our client’s IRAs and brokerage accounts. For more about our wealth preservation services, visit our website. Our monthly Investment Analysis Report requires a subscription fee of $40 a month. Current subscribers are allowed to freely distribute this report with proper attribution.

Copyright ©2007 Lamont Trading Advisors, Inc. Paul Lamont is President of Lamont Trading

Advisors, Inc., a registered investment advisor in the State of Alabama.

Persons in states outside of Alabama should be aware that we are relying on de

minimis contact rules within their respective home state. For more information

about our firm visit http://www.ltadvisors.net,

or to receive a copy of our disclosure form ADV, please email us at advrequest@ltadvisors.net,

or call (256) 850-4161.